FOR EVERY PURCHASE OF ₹ 2000 OR MORE, WE WILL PLANT ONE TREE TO SUPPORT OUR GROWTH INITIATIVE.

FOR EVERY PURCHASE OF ₹ 2000 OR MORE, WE WILL PLANT ONE TREE TO SUPPORT OUR GROWTH INITIATIVE.

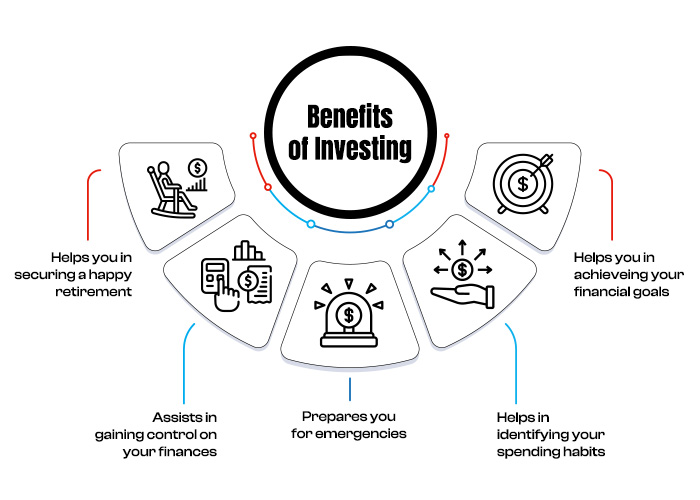

Wondering how soon you can invest and grow wealth in the future? Think about all the right steps to be followed for your right investment plan, where you can create the wealth that you need in the long run. The classic board game Othello reflects this in its tagline, “A minute to learn… a lifetime to master.” This single statement could apply to the task of choosing your investments. Understanding the basics doesn’t take long, but mastering the nuances can take a lifetime.

Investment strategies matter in your “rags to riches” story, and if you are one of those who want to invest now, strategic planning can help. In this blog, we will discuss some basic concepts that any investor should focus on if they want to improve the effectiveness of their investment selection.

The Key Step: Knowing Your Goals

There’s never been the best investment strategy. Every investor’s goal is different. One might want to invest for 10 to 15 years, while another might be looking for 20 to 25 years. The question that you need to ask yourself is, “When do I need the money?” This is constantly changing based on your needs, desires, and uncertainties. Depending on the goal-setting you do, you can choose from among PPF, fixed deposits, mutual funds, and ULIP. Most people believe that short-term savings can help them achieve their goals sooner than long-term savings. However, cultured investors believe in letting your money sit for a long time to give you the desired returns.

Assessing your risk-taking abilities

Every aspect of life leads to a decrease in an individual’s appetite or ability to take risks, as aging often brings with it changes in roles and responsibilities, as well as preferences for when and where to invest. We can determine how to enter the market, book profits, and exit when our investment goals align with our risk-bearing ability. Now that we know where our risk forbearance lies, we look at the strategic factors that play a vital role in defining how one can invest.

The essential ingredients to successful investing

Knowing your timeline

You should commit your investments to a period where you will not touch them. When you invest for the long term, you can expect a reasonable rate of return because you are evaluating the profits over a longer time horizon. When investors have time on their side, they are more likely to appreciate and weather the inevitable ups and downs of the equities market.

“Trusting the Magic of Compounding”

When people cite “the snowball effect,” they’re talking about the power of compounding. Another important reason to leave your investments untouched for several years is to take advantage of compounding. Compound growth occurs when you start earning on the money your investments have already earned. This is why many start investing early just to outperform late starters. They get the benefit of compounding growth over a longer period of time.

What is the right asset class for you?

The best investment strategy is one where you put your funds into several types of asset avenues, each representing a percentage of the whole. Over time, diversifying risk has proven to be highly effective by allocating assets into different classes that do not exhibit strong price correlation.

For example, invest half of your money in stocks and the other half in bonds.

To know the right allocation strategy for you, you need to understand your tolerance for risk. Lower-risk options like bonds are a bit on the defensive side, whereas if you can go aggressive, look for mid- and small-cap stocks.

The taste of diversification

Choosing among various asset classes doesn’t just manage risk. According to Harry Markowitz, the Nobel Prize-winning economist who coined reward as “the only free lunch in finance,” You earn more if you diversify your portfolio. Diversification brings greater rewards.

According to Harry Markowitz, let’s assume an Indian investor has INR 10,00,000 to invest. Instead of putting all the money in one asset class, they decide to diversify their portfolio.

- Equities: Invest 40% (INR 4,00,000) in a diversified equity fund consisting of large, mid, and small-cap stocks across various sectors.

- Debt: Invest 30% (INR 3,00,000) in a mix of government and corporate bonds with varying maturities.

- Gold: Invest 15% (INR 1,50,000) in gold ETFs or physical gold.

- Real Estate: Invest 15% (INR 1,50,000) in real estate through REITs or direct property investments.

By diversifying across these asset classes, the investor reduces the impact of any single asset’s performance on the overall portfolio. If the stock market declines, the gains from debt or real estate might offset the losses.

Traditional and Alternative Assets: A blended approach always works better.

Most financial professionals broadly divide all investments into two categories: traditional assets and alternative assets.

- Traditional assets include stocks, bonds, and cash. Cash in the bank includes savings accounts and certificates of deposit.

- Alternative assets are everything else, including commodities, real estate, foreign currency, art, collectibles, derivatives, venture capital, special insurance products, and private equity.

For most individual investors, a combination of stocks and bonds, plus a cash cushion, is ideal. For others with highly specialized knowledge, they tend to look for other avenues. If you’re an expert on antique Portuguese artifacts, you should buy them. If you’re not, you’re better off sticking with the basics.

Balancing between Bonds and Stocks

If most investors can reach their goals with a combination of stocks and bonds, then the ultimate question is, how much of each class should they pick? Let us see the pattern followed globally.

A risk-averse investor may be uncomfortable with even short-term volatility and choose the relative safety of bonds, knowing the return will be lower.

In his book Stocks for the Long Run, author Jeremy Siegel makes a powerful case for designing a portfolio consisting primarily of stocks. If you want a higher return and can tolerate the higher risk, mostly stocks are the way to go. The fact is, the total return on stocks historically has been much higher than for all other asset classes.

But the question is, how do you pick stocks?

Now that we can see that stocks offer higher long-term appreciation than bonds, let’s look at the factors an investor needs to consider when evaluating shares.

- Dividends: Dividend payments are a sign of a healthy company, and dividends are a powerful way to boost your earnings. The company’s discretion determines the frequency and amount of the dividend, primarily based on its financial performance. More established companies typically pay dividends.

- P/E Ratio: A price-earnings ratio is the company’s current share price compared to its earnings per share. The P/E ratio is the most commonly used measure of a stock’s relative value. A high P/E ratio indicates that investors have greater expectations for a company. A low P/E ratio could suggest that investors undervalue the company or anticipate more challenging times ahead.

- Beta: This number indicates the volatility of a stock in comparison to the market as a whole. A security with a beta of 1 will exhibit volatility that’s identical to that of the market. Any stock with a beta below 1 is theoretically less volatile than the market. A stock with a beta above 1 is theoretically more volatile than the market.

- Earnings Per Share (EPS): A company allocates a portion of its earnings, after taxes and preferred stock dividends, to each share of common stock. Investors can use this number to gauge how well a company can deliver value to shareholders. A higher EPS begets higher share prices. The number is particularly useful in comparison to a company’s earnings estimates. If a company regularly fails to deliver on earnings forecasts, an investor may want to reconsider purchasing the stock.

- Historical Returns: As the investing brochures always phrase it, “Past performance is not a predictor of future returns.” Investors often get interested in a stock after reading headlines about its phenomenal performance. Just remember, that’s just news. Sound investing decisions should consider context. A look at the trend in prices over the previous 52 weeks, at least, is necessary to get a sense of where a stock’s price may go next.

Technical and Fundamental Analysis

You can process different types of investments in your portfolio using either technical or fundamental analysis. Let’s look at what these terms mean, how they differ, and which one is best for the average investor.

Technical Analysis

With the help of enormous volumes of data, technical analysts comb through it in an effort to forecast the direction of stock prices. The data consists primarily of past pricing information and trading volume.

These folks are not interested in monetary policy or broad economic developments. Their primary philosophy is that prices follow a pattern, and if they can decipher the pattern, they can capitalize on it with well-timed trades.

In recent times, technology has become a more reliant practice of investing because the tools and the data are more accessible than ever.

Fundamental Analysis

Fundamental analysts are the species that consider a stock’s intrinsic value. Their identification is based on the industry’s prospects, company management quality, revenues, and profit margin.

Many of the concepts discussed throughout this piece are common in the fundamental analyst’s world.

Technical analysis is best suited to someone who has the time and comfort level with data to put limitless numbers to use. Fundamental analysis, on the other hand, caters to the majority of investors and offers the advantage of practical application.

Then what’s the best plan?

It is true that with more investment risk and fluctuating market conditions, an investor tends to fumble and choose one with a lower risk of market growth. If great investors inspire you, keep in mind that their success stems from the strategies they employed and the returns they generated from their investments. One point that every successful investor advocates for investing in a high-risk profile if their goal is long-term, as higher risk typically yields higher returns over time. goal is short-term, investing in a low-risk portfolio makes more sense. Depending on the risk, your appetite for profit and loss, and the income sources at your disposal, you can choose something that suits your needs and wants while also not hurting your pocket badly. Using all the above-mentioned strategies smartly, you can attain financial freedom; the choice is yours.

eV7W5z33yiZ

I?¦ll immediately take hold of your rss feed as I can not to find your e-mail subscription hyperlink or newsletter service. Do you’ve any? Please permit me recognize in order that I may just subscribe. Thanks.

Really enjoyed this article, can I set it up so I receive an alert email whenever you publish a fresh update?